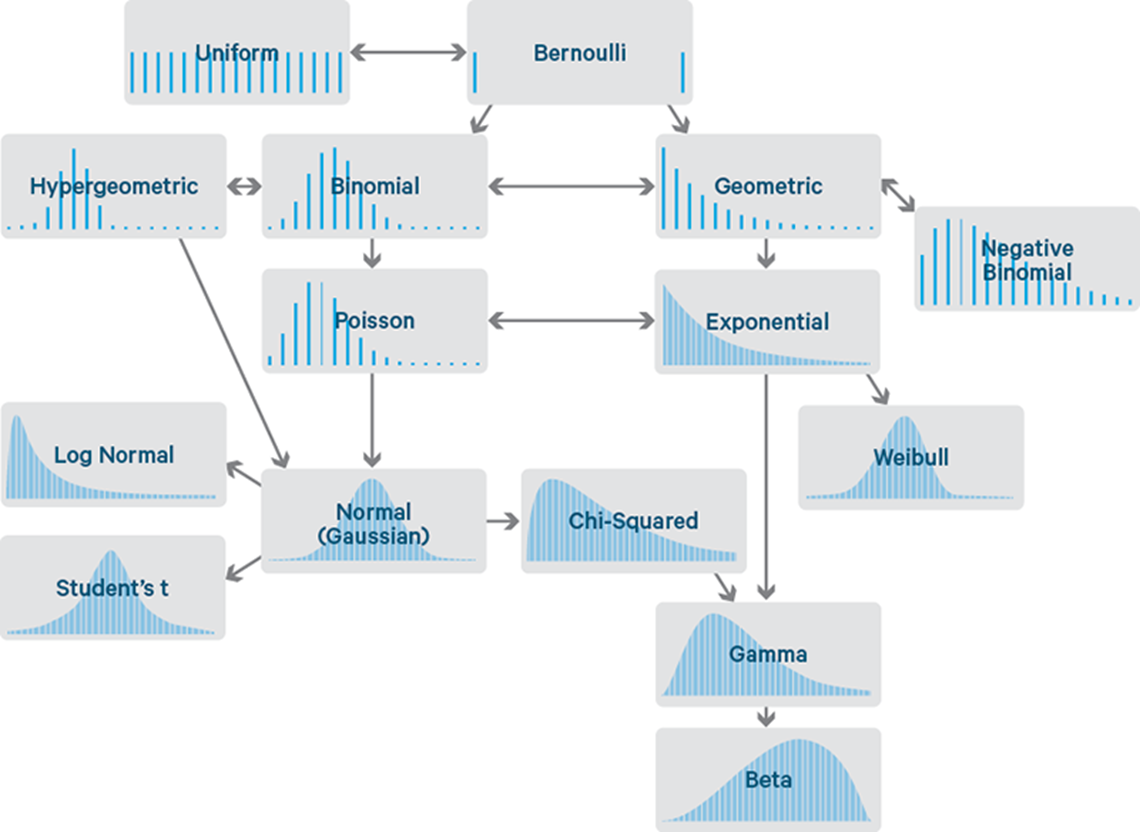

Descriptive Analytics - Probability distributions

Codes on Google Collab

Predictive analytics VS randomness

- What is a prediction?

- Is prediction possible?

- What do we predict?

Bernoulli trial

- A random experiment with only two possible outcomes:

- “Success” and “Failure”

- Red and Black, Head and Tail, win or lose

- Customer renewed subscription, made a purchase, repaid a loan, or not

- Probability of “success” 𝑝 is always the same

- 𝑝=1−𝑞,

- 𝑞=1−𝑝,

- 𝑝+𝑞=1

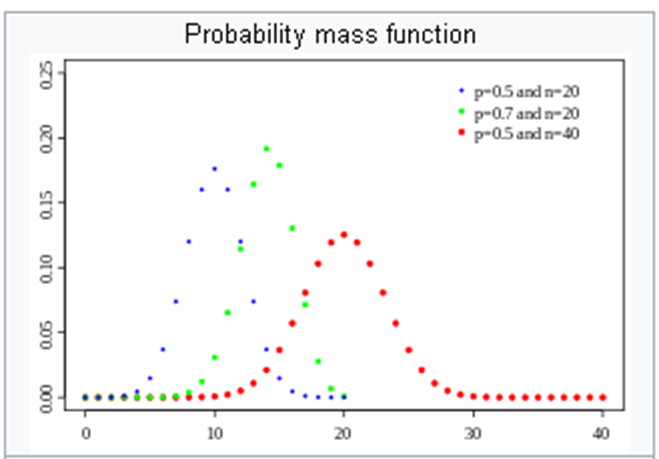

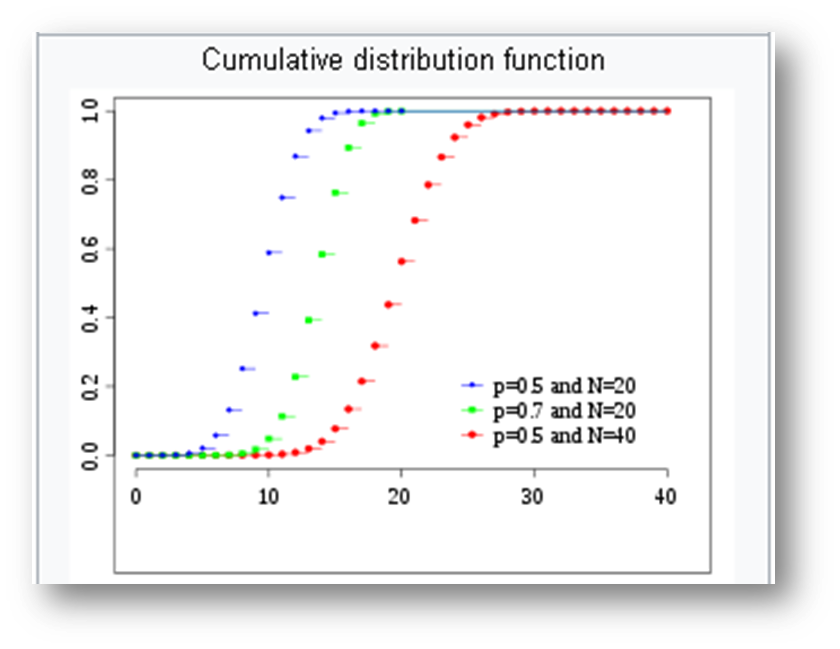

Binomial distribution

- 𝑛 random independent Bernoulli trials with fixed probability of “success” 𝑝

- Let 𝑋 be the number of successes after 𝑛 trials

- Where

- Other notations are

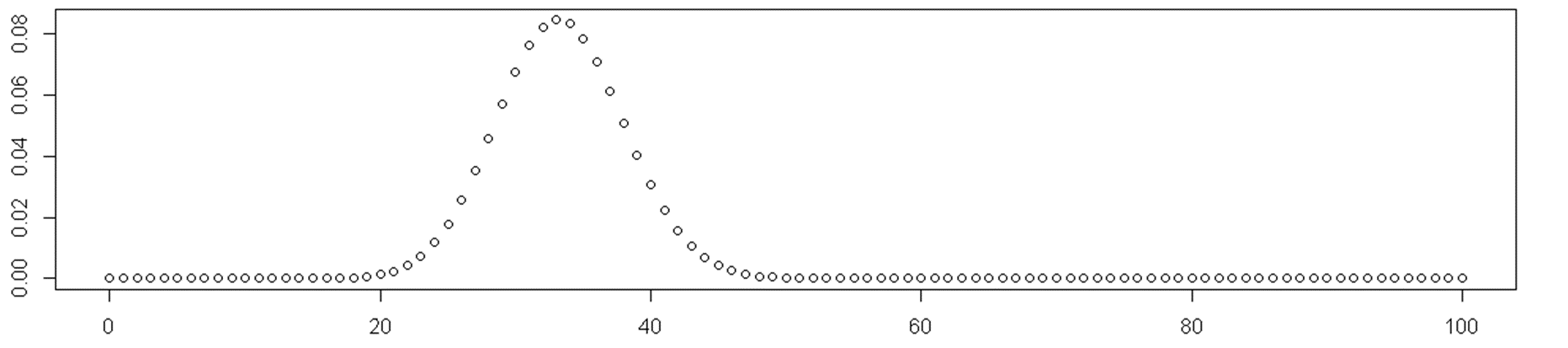

Example 1

- A test with 10 multiple-choice questions. Each question has three possible answers.

- Let’s assume that student does not know the topic at all, then the probability to get the right answer in a question is

- What is an expected result for this student?

What is a probability this student passes the test (gets 50% or more)?

1-sum(dbinom(seq(0, 4), 10, 1/3))What is a probability this student passes the test with 100 questions?

1 - sum(dbinom(seq(0,49),100,1/3))

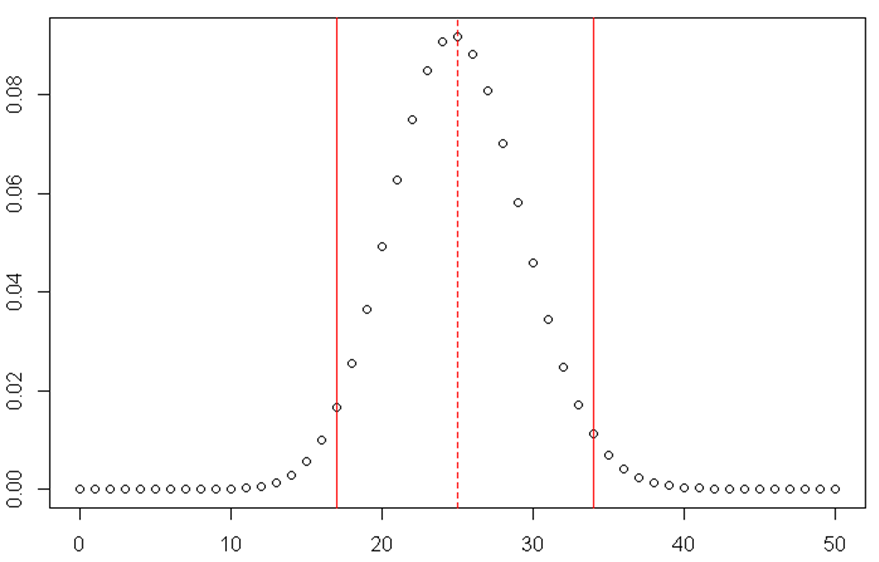

Example 2

- Customers arrive to your store. You know that approximately one in four customers will buy your product, while others just shop around.

- How many units will you sell if there are 100 customers per day?

- What are upper and lower bounds for the number of units sold?

qbinom(c(0.025,0.5,0.975),100,1/4)

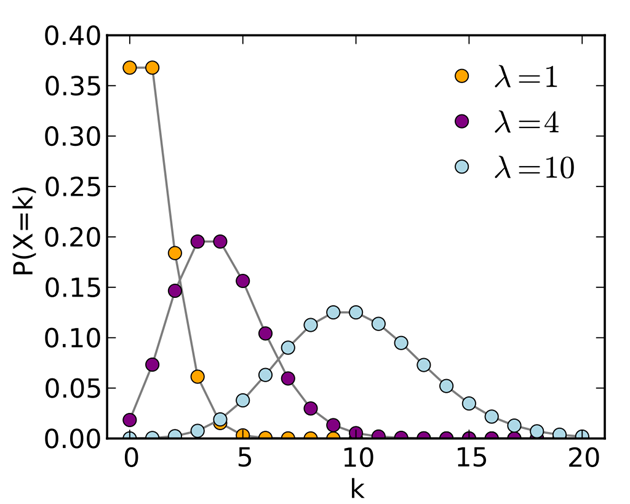

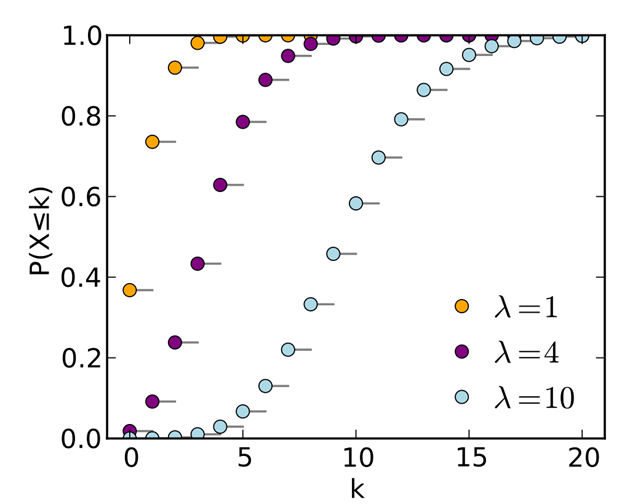

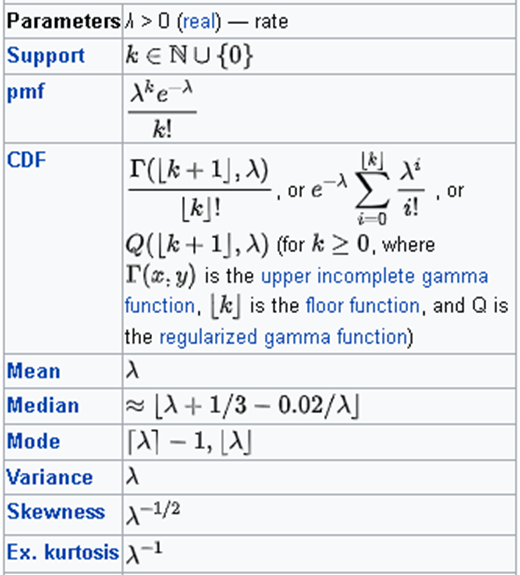

Poisson distribution

- Events occur independently, at random, at a rate 𝜆 per unit time. We want to count the number 𝑋of events happening in a given time 𝑡.

Example

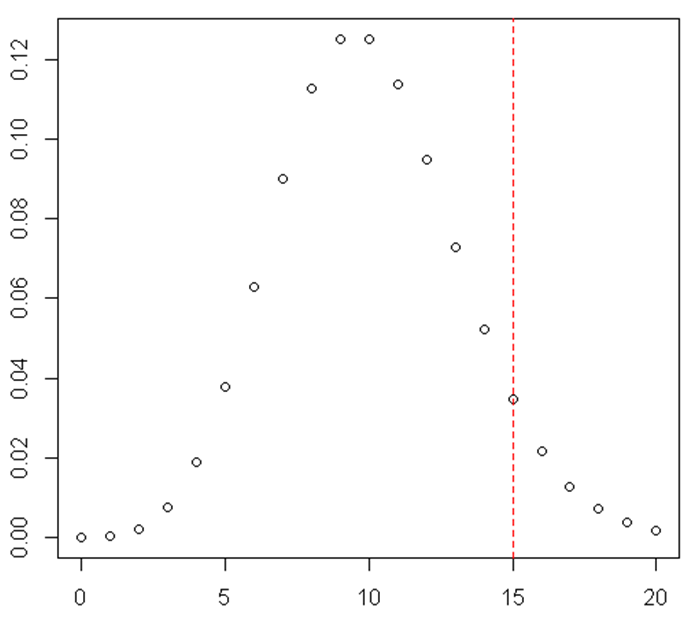

There are 10 customers arriving to your store every day IN AVERAGE. What is probability that on some day there would be 15 customers or more?

1-sum(dpois(seq(0, 14), lambda=10))The Poisson distribution is often described as “the distribution of small numbers”.

Negative Binomial Distribution

- There is a sequence of independent and identically distributed Bernoulli trials with probability of success 𝑝.

- We want to know the number of successes happen before 𝑟 failures.

Example:

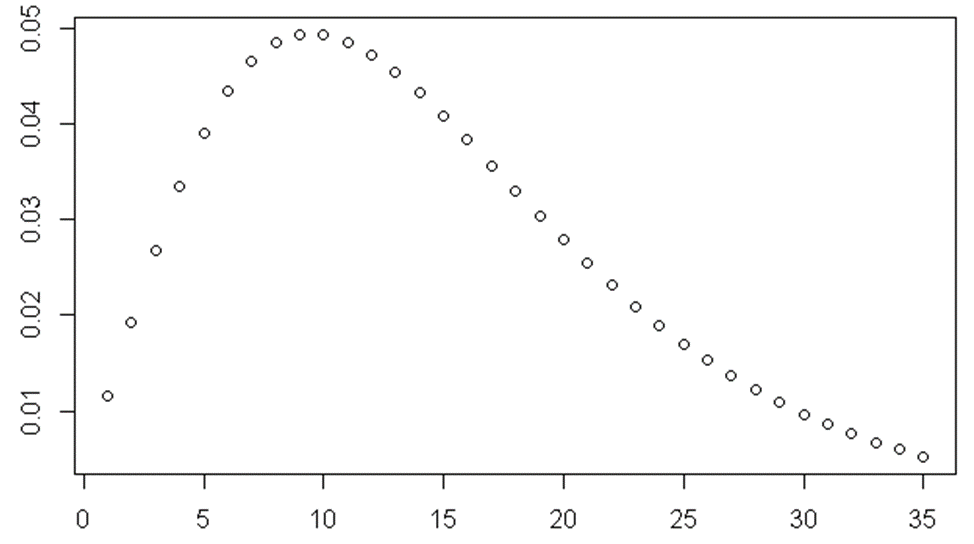

- We roll a dice and consider number “1” as failure and any other number as a success. That is, 𝑝=5∕6

- How many “successes” do we get before getting three failures, that is, before we see “1” in a third time, so 𝑟=3

plot(dnbinom(seq(1,35), size=3, prob=1/6))

- “Overdispersed Poisson”

- A mixture of Poisson distributions, where rate 𝜆 is itself a random variable, distributed as a gamma distribution with shape 𝑟 and scale 𝜃=𝑝(1−𝑝)

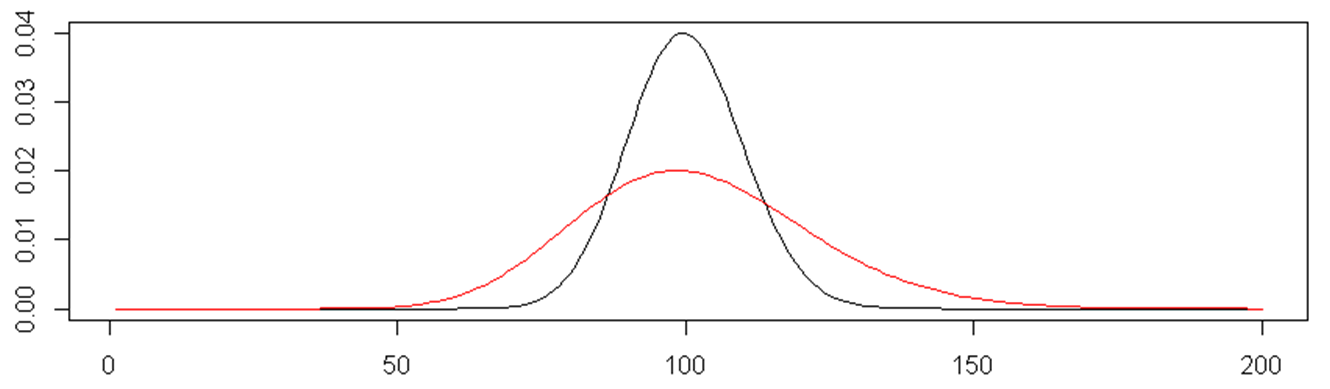

plot(dpois(seq(1,200), lambda=100), type="l")

lines(dnbinom(seq(1,200), size=34, prob=0.25), col="red")Examples

- Number of job interview you have to go on before you get a job

- Number of patients arriving to Hospital Emergency Department

- Number of customers coming to supermarket

- Occurrence of tropical cyclones in North Atlantic and winter cyclones over Europe

- How long an engine part will work till it gets broken and need replacement or repair

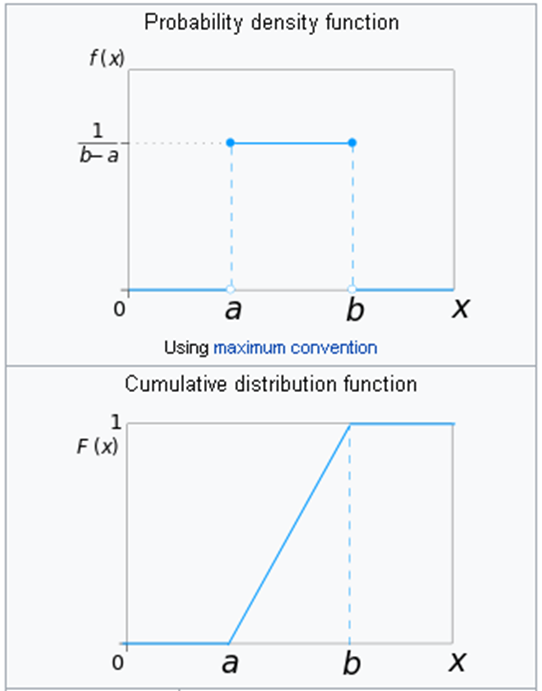

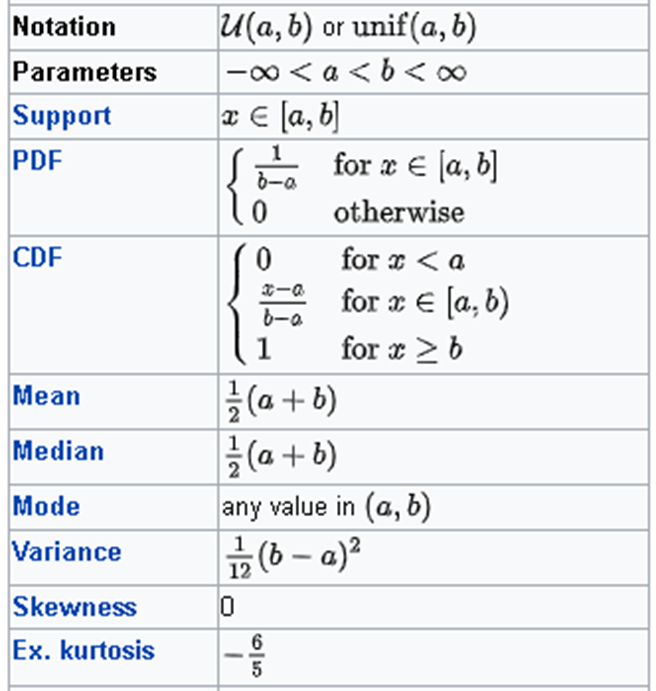

Uniform distribution

x <- sample.int(6, size=6000, replace=TRUE)

plot(table(x))

abline(h=1000, col="red", lty=2)x <- runif(6000)

hist(x, breaks=10)

abline(h=600, col="red", lty=2)Uniform distribution (continuous)

Very often we say that [variable] is “uniformly distributed”

- if customers show no preferences towards any particular product

- if there is no effect of on the variable from the selected predictors

- If there is no difference between groups

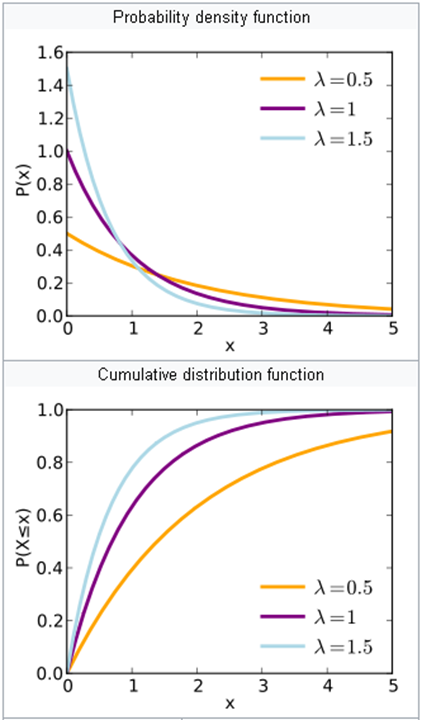

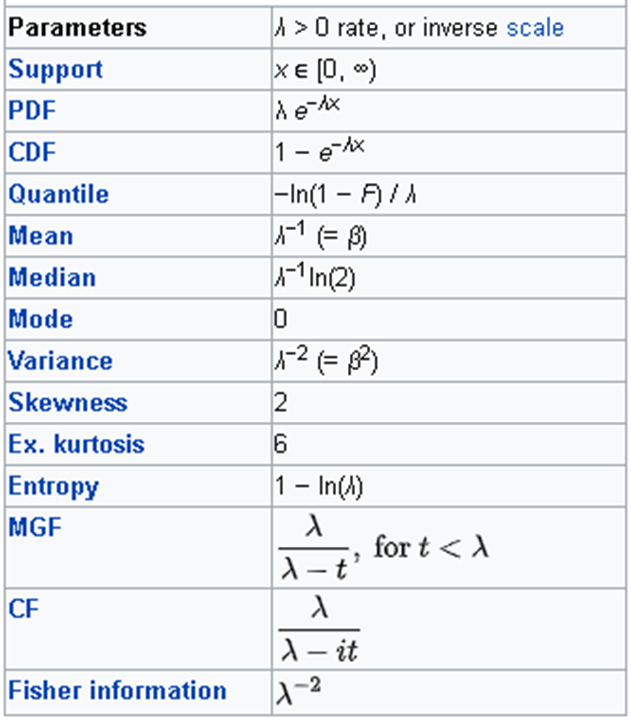

Exponential distribution

If we assume that events occur according to Poisson distribution with a rate 𝜆 then waiting time 𝑇 before [next] event follows exponential distribution

Example

Exponential distribution can be used to estimate time between different kinds of events:

- Time between jobs arrivals to a service centre

- Time to a component failure (lifetime of a component)

- Time required to repair a component

- How long to wait for the next phone call

- How long to wait for a next customer to arrive

Paradox

- Suppose you join a queue in a bank, with just one customer in front of you, already in service.

- The time you have to wait for that customer to finish being served is independent of how long that customer has already been in service!

- Exponential distribution is memoryless.

- If you have been waiting time 𝑠 for the first event, what is probability that you will wait a further time 𝑡?

Hence, your remaining waiting time does not depend on time 𝑠 you already have been waiting.

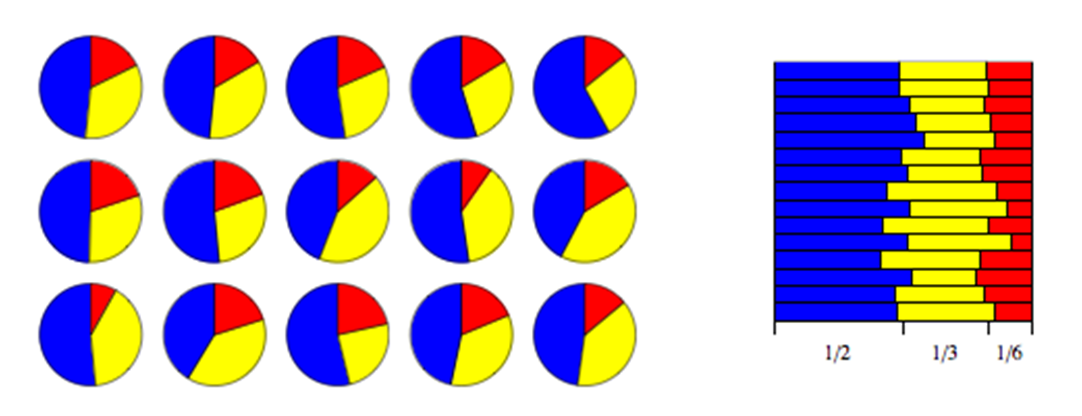

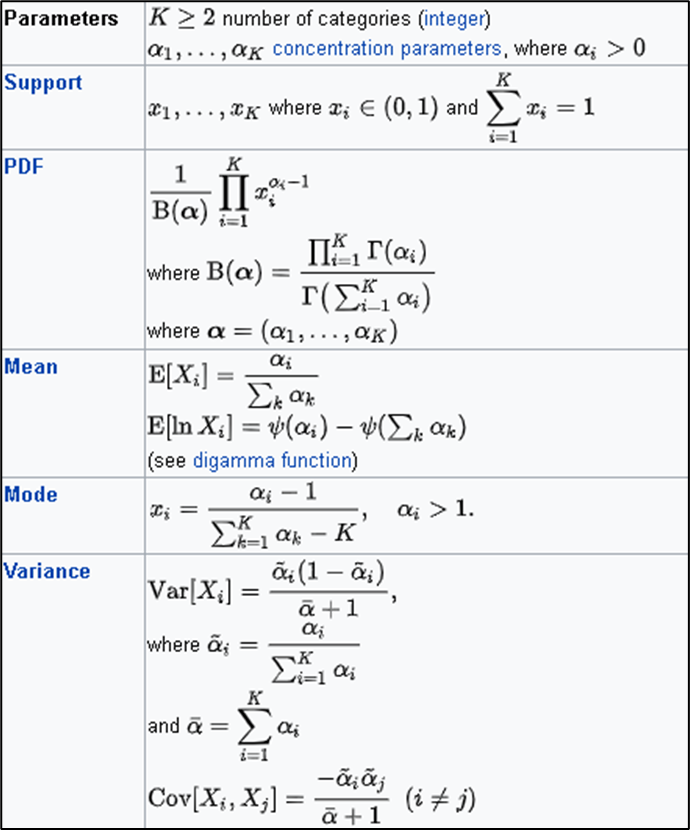

Dirichlet distribution

Market share:

Company A – 50%

Company B – 33%

Company C – 17%

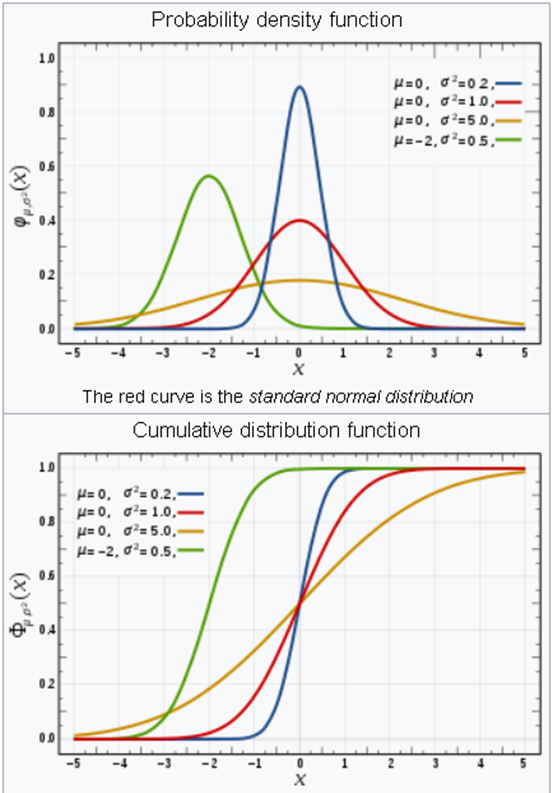

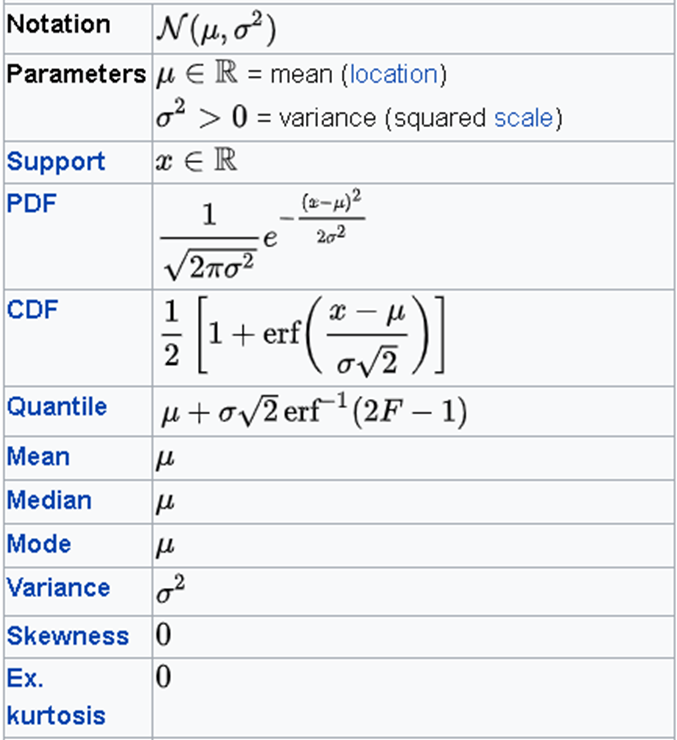

Normal Distribution

- Gaussian distribution

- Continuous two parameter distribution

- Arises in many biological and sociological experiments

- Limiting distribution in many situations

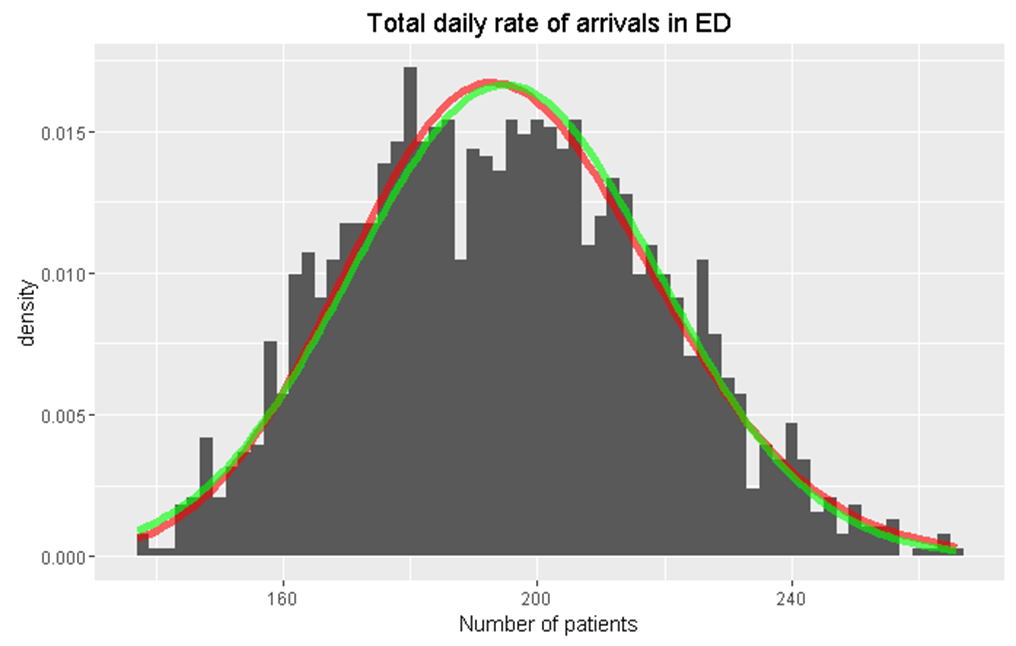

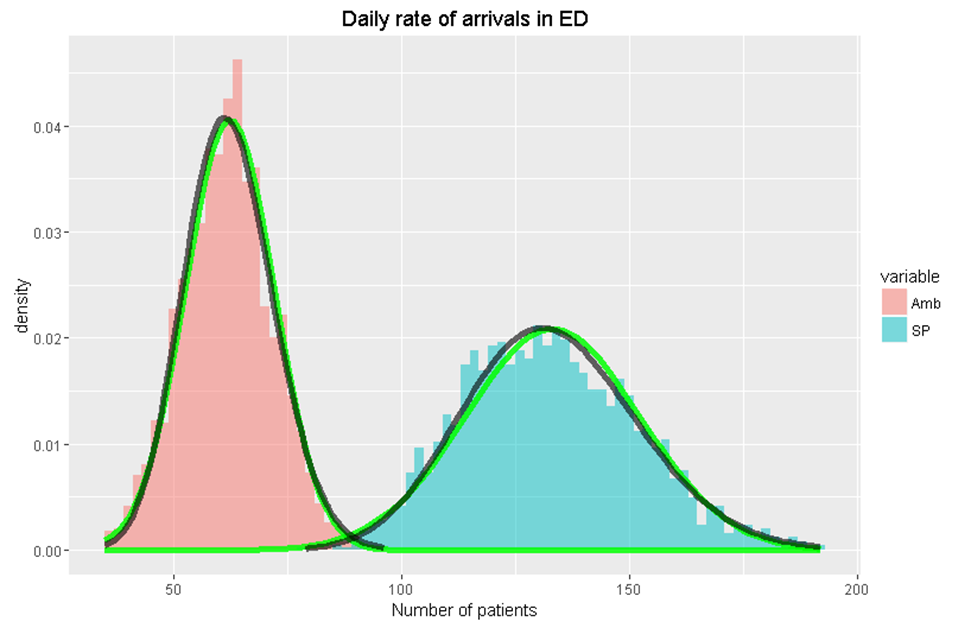

df <- data.frame(PF = rpois(1000, lambda=50))

ggplot(df, aes(x = PF)) +

geom_histogram(aes(y =..density..), binwidth=2) +

stat_function(fun = dnorm,

args = list(mean = mean(df$PF), sd = sd(df$PF)),

col="red", size=2)df <- data.frame(PF = rnbinom(1000, size=34, prob=0.25))

ggplot(df, aes(x = PF)) +

geom_histogram(aes(y =..density..), binwidth=5) +

stat_function(fun = dnorm,

args = list(mean = mean(df$PF),

sd = sd(df$PF)),

col="red", size=2) +

stat_function(fun = function(x) dpois(as.integer(x),

lambda = mean(df$PF)) ,

color = "green", size = 1)x <- matrix(runif(120000),10000,12)

df <- data.frame(PF=apply(x,1,sum)-6)

ggplot(df, aes(x = PF)) +

geom_histogram(aes(y =..density..), binwidth = 0.1) +

stat_function(fun = dnorm,

args = list(mean = mean(df$PF), sd = sd(df$PF)),

col="red", size=2)x <- matrix(rexp(120000),10000,12)

df <- data.frame(PF=apply(x,1,sum))

ggplot(df, aes(x = PF)) +

geom_histogram(aes(y =..density..), binwidth = 1) +

stat_function(fun = dnorm,

args = list(mean = mean(df$PF), sd = sd(df$PF)),

col="red", size=2)Mixture distribution

Non-homogenous distributions

- Let’s assume that cars arrive at an intersection with some rate 𝜆 cars per hour.

- Now, assume that 𝜆 is not constant but a function of time 𝜆(𝑡). That is, more cars during the day and less during the night.

- Arrivals process is a non-homogenous Poisson process.

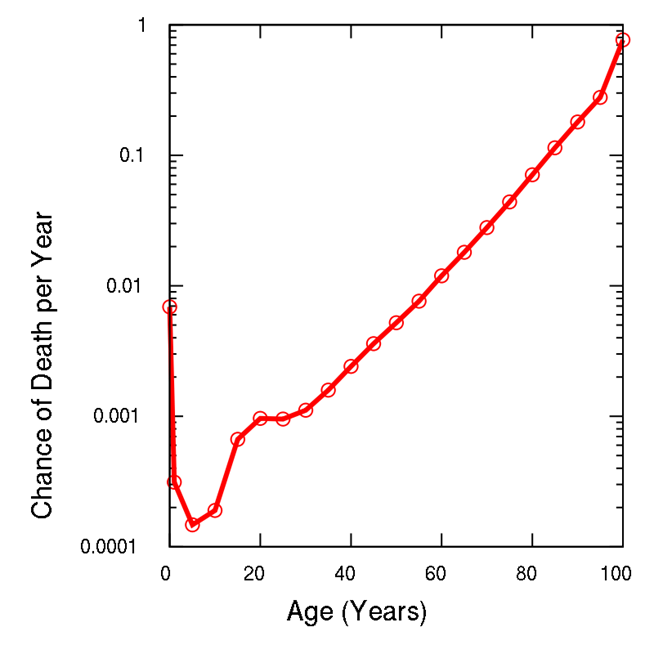

- Time of arrival becomes not exponential but somewhat different, depending on the function of time 𝜆(𝑡). Often used in actuarial science, e.g. see Gompertz–Makeham law of mortality

Non-parametric distributions

- Parametric distributions are distributions that can be completely described by their parameters, like 𝑁(𝜇, 𝜎^2).

- Non-parametric or empirical distributions do not assume that data drawn from any known parametric distribution

Summary

Predictions about data:

- central tendency,

- dispersion,

- most popular,

- max or min values.